A major lender in the mortgage market is showing signs of strain, according to research conducted by Legal & General with the Centre for Economic Business Research.

The study reveals 27 per cent of house purchases would not happen without this lender’s help, but predicts that its 2018 lending will fall to £5.7bn, down from £6.5bn in 2017.

The drop in lending by this institution, made up of parents, grandparents, friends and other relatives – otherwise known as the ‘Bank of Mum and Dad’ (Bomad) – reflects tougher economic conditions and a squeeze on household income, the research suggests.

While house price growth has slowed to its weakest level since 2012, prices remain high relative to earnings. They are expected to continue their upward trend, albeit at a slower pace. Sluggish wage growth and the rise in interest rates in November 2017 have also contributed to the mixed backdrop. Consequently, Bomad’s contribution to would-be homebuyers has fallen from an average of £21,000 last year to an estimated £18,000 in 2018. But while the overall amount lent has fallen, the number of borrowers helped is predicted to rise from 298,300 to 316,600. That represents around a quarter of transactions, equivalent to £82bn of lending in England and Wales.

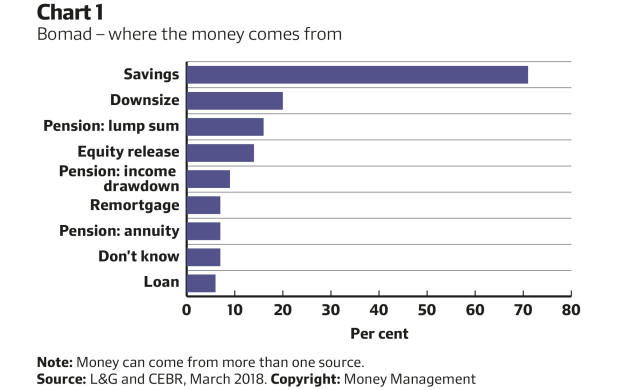

Whether the issue is low pay, higher inflation or high house prices, it is clear that parents and other family members have less cash to spare. More than 70 per cent used cash savings to help their loved ones get on to the housing ladder, while 20 per cent downsized their homes, and 16 per cent used a lump sum from their pensions. Only 10 per cent said giving the money made them feel financially less secure, but nearly 20 per cent said they had to cut back in some way, perhaps by foregoing a holiday or car purchase as a result of giving the money.

The age of borrowing

The study shows that 27 per cent of buyers will receive financial help from friends and family in 2018, up from 25 per cent in 2017. While most of those receiving help from Bomad are relatively young, there are exceptions. Nearly 60 per cent of borrowers under 35 received help, but so did 43 per cent of those aged 35 to 44, and 26 per cent of those aged 45 to 54.

The report expresses surprise that people of this age are having to rely on parents and relatives for help to buy a house at a time when their earnings are likely to be at a peak and they have children of their own. Nevertheless, it suggests this reveals the age at which people are able to buy their homes has increased significantly as house prices have risen. It also reflects the challenges of “second steppers” – those already on the housing ladder looking to upsize but struggling to raise enough money. It concludes: “For every age group [looking to buy], outside help looks set to remain crucial.”

Chart 1 shows the different sources of funds used to help Bomad borrowers. L&G, an equity release lender itself, is keen to consider the use of equity release by Bomad. Only 4 per cent of over-55s in the UK used it in 2018, but 39 per cent said they might consider doing so. Of those, nearly half said they would use the money to help a friend or relative buy their own home. Were they to follow through on that consideration, this segment would become one of the biggest drivers of equity release, putting it ahead of the likes of property renovation, currently a catalyst.