When investing in fixed income markets, investors will want to understand where they should be positioned on the yield curve and the correlation between risk and yield.

Generally speaking, the higher the yield, the more risk an investor is taking because the quality of the credit is lower.

Ben Edwards, fixed income manager at BlackRock, explains investors need to think about two distinct curves when investing in bonds.

“Firstly, the credit curve, which is generally well understood – the lower the quality of the issuer, the higher the yield. That higher yield compensates investors for an increased probability that a company will fail to meet its financial obligations,” he says.

“Less well understood is the important effect the maturity curve can have on the returns of bonds.

“Irrespective of the current quality of a particular company, its revenues, costs, management team, strategic direction and financial policy all become less certain as time goes on. For this reason, corporate bonds tend to pay a higher yield for longer maturities.”

He explains how this works in practice, using corporate bonds as an example.

“The longer end (those with maturities above 15 years) of the sterling corporate bond market offers a poor risk/reward trade off,” Mr Edwards notes. The additional compensation to own a BBB sterling bond with a maturity of 30 years is only 0.3 per cent higher than that of 15 years.

“For that, investors take on additional asset volatility and give up considerable certainty of the direction of the company. That additional yield could more easily be captured by buying seven-year bonds rather than five-year bonds, for example.”

He continues: “And for that reason, the six to 10-year part of the maturity curve offers strong relative risk-adjusted returns.

“By selecting bonds whose yields are expected to fall more quickly as they progress toward maturities, investors can earn above-market returns and avoid the volatility of longer maturity bonds.”

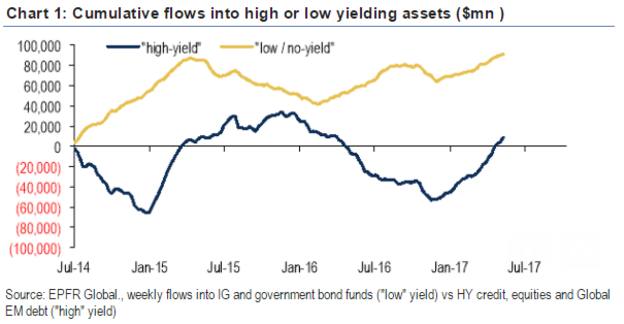

Figure 1: Cumulative flows into high or low yielding assets ($m)

Source: EPFR Global, BofA Merrill Lynch

Predicting the future

But given investors have become used to being in a bond bull market for many years, what should they expect from future returns from bonds?

With such a close relationship between interest rates, inflation and bonds, investors will have to consider their duration positioning, as Ben Willis, head of research at Whitechurch Securities points out.

Those who believe interest rates are on an upward trajectory will be positioned differently from those who think interest rates will stay where they are or get lower.

Mr Willis says: “If you believe that interest rates and/or inflation numbers are going to increase more rapidly than consensus, then you will be focusing on short duration bonds and will be prepared to accept a lower yield as your concern will be a drop in bond prices.